Common Love for Data

We recognize the importance of using vast data sets to make better informed investment decisions – so our research budget is skewed more aggressively toward data procurement and analytics. We believe data matters and have invested heavily in sourcing the best data from which we can extrapolate the best insights.

On-location Research

We are making a strategic return to our roots by increasing our “on-location” research. Classical research was once balanced between C-level interactions and bottom-up, factory level analysis. As analysts have added stocks and responsibilities, the latter has fallen off sharply. We intend to do more of the bottom-up research by increasing visits to off-circuit trade shows and spending more time with private companies.

Corporate Access

We aim to change the corporate access model by providing a higher level of connectivity and engagement between corporates and our clients. We believe through small-group settings and corporate tours, we can provide more meaningful access for our clients. Our annual Industrial Tech & Aerospace Forum has quickly become a must-attend industry event combining leading corporate management teams with industry experts, consultants, and disruptive tech private companies. This year’s forum will take place June 18-19 in New York City.

Market-Tested Experience

Our experience is a competitive advantage. Our collective success on a historical basis is solid, but as important are our past failures that will help us generate better insight going forward. Our investment process will evolve with technology. As a smaller, more focused research shop, we can adapt very quickly and continuously improve, which we will strive to do each and every day.

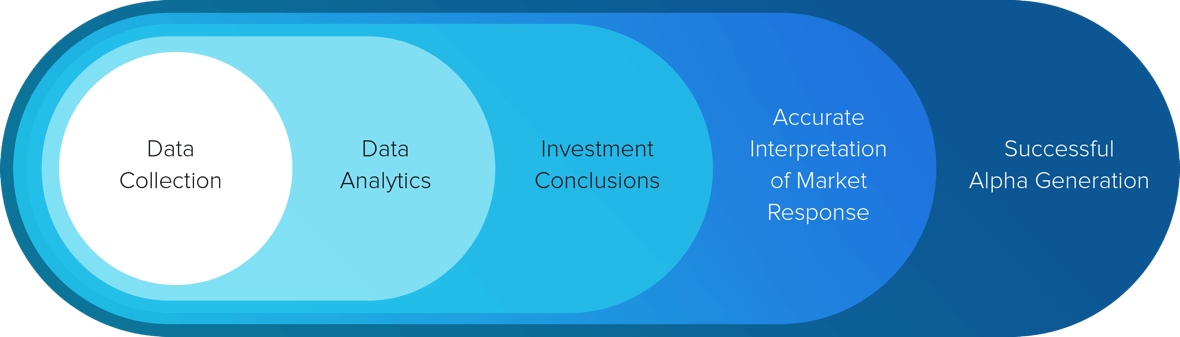

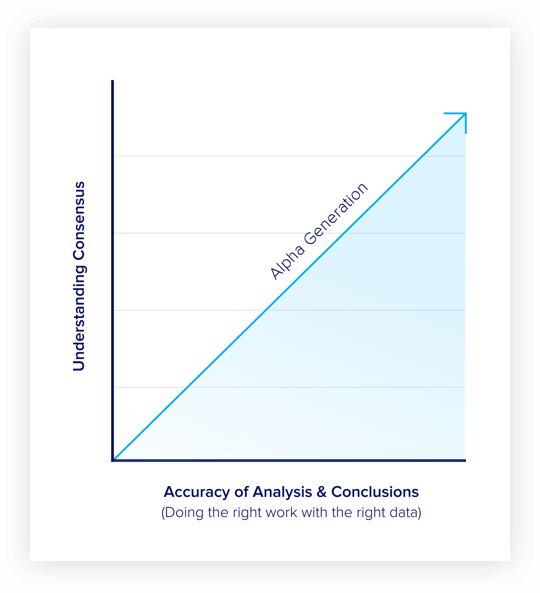

Right Work + Right Data

We see two categories of mistakes one can make in the investment selection process: errors of omission and errors of judgment. Errors of omission are caused by doing the wrong work, or not doing the work at all. Errors of judgment come from inaccurately forecasting how the market will respond to results or a data set. Our work is focused on doing the right work with the right data, and therefore, is intended to decrease the odds of failure of omission. If we can maximize accuracy of the first variable, then minimizing errors of judgment can simply boil down to understanding sentiment — largely just a variable solved by listening more than talking.